Table of Content

This is where the lender must go through the courts to get permission to foreclose by proving the borrower is delinquent. Foreclosure is a legal process that allows lenders to recover the amount owed on a defaulted loan by taking ownership of and selling the mortgaged property. If those payments cannot be made, and the borrower defaults on the home loan, the deed remains in possession of the lender, who can legally take back ownership of the home used as collateral, in order to cover their loss.

That's why a foreclosure can be devastating for homeowners who are facing financial hardships. Through the foreclosure process, lenders are able to seize ownership of a property when the borrower has defaulted on their mortgage. With chapter 13 bankruptcy, lenders are required to halt any impending foreclosure proceedings. In most cases, homeowners are given a period of time to fix their finances and repay the lender before any action can be taken. In some states, borrowers have up to 5 years to resolve their delinquencies, and even then, some states require the lender to actually file a lawsuit against the borrower in order to collect the money owed.

Home.loans Knowledge Base

At this point, the more time that a borrower has spent in delinquency without making any payments, the harder it is to catch up with the payments, making it incredibly hard to stop the foreclosure process. Banks usually dispirit borrowers to prepay housing loans as the borrower would end up repaying lesser to the bank than if he/she had to finish off the entire tenure of the loan. Closing off a loan before the term is due allows the borrower to evade a part of the interest. Any interest he/she was supposed to pay post preclosure will automatically be waived off on closing the loan.

The successful bidder must pay the full amount of the bid immediately with cash or a cashier’s check. The successful bidder gets a trustee’s deed once the sale is complete. The lender usually bids at the auction, in the amount of the balance due plus the foreclosure costs. If losing the home doesn’t seem like too much of a problem, homeowners can always try to request a mortgage release or sell the home in a short sale.

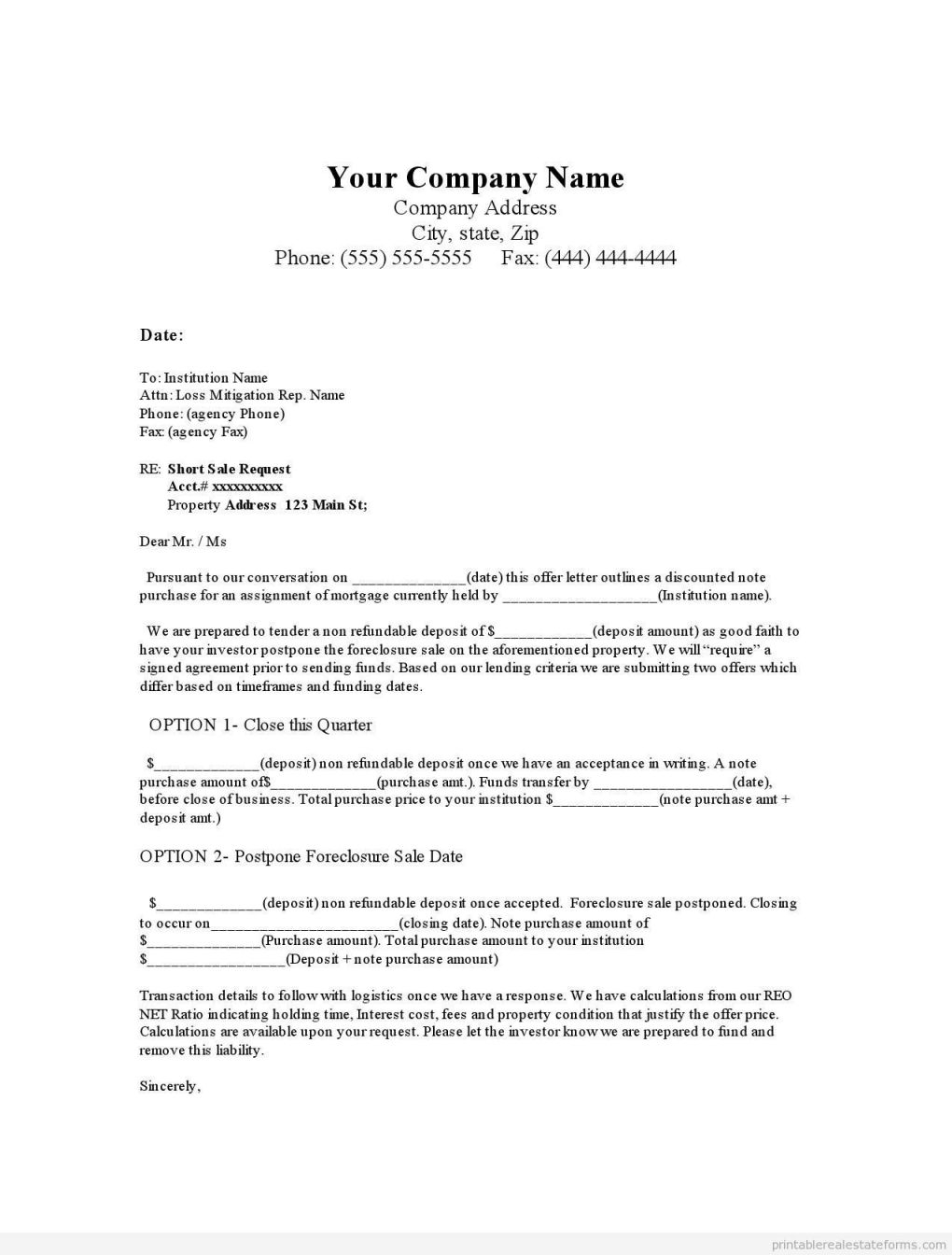

Short Sale

Typically, mortgage payments are due on the first day of each month, and many lenders offer a grace period until the 15th of the month. After that, the lender may charge a late payment fee and send the missed payment notice. Foreclosure is the process that allows a lender to recover the amount owed on a defaulted loan by selling or taking ownership of the property. Although the foreclosure process varies by state, there are six common phases of a foreclosure procedure. Foreclosure occurs when a homeowner is no longer able to make mortgage payments as required. This allows the lender to seize the property, removing the homeowner and selling the home, as stipulated in the mortgage contract.

Only in the absolute rarest of cases do companies release borrowers from delinquencies free and clear, so you can count on any payments that were suspended or any reduction amounts to be due at a later date. In fact, forbearance can actually be a danger to some homeowners, as many forbearance deals come with a balloon payment that might be hard to afford on its own, and might even put a homeowner back at risk for foreclosure. Pre-foreclosure is a period that can last anywhere between 3 to 10 months.

Guide Taxonomy

Reinstatement—During the reinstatement period, the borrower can pay back what they owe before a specific date to get back on track with the mortgage. And in the event that the penalty on preclosure exceeds the interest saved on the loan, it becomes irrational to preclose the loan. An acknowledgement of the payment made towards the loan must be taken from the bank. A cheque book must also be kept handy as you may need to pay the final settlement of the housing loan. If you’ve seen a foreclosure action, successful or not, or if you have any comments or questions, please let us know in the section below. Depending on the state, foreclosures can occur as quickly as 30 days, and up to seven months .

The lenders place a lien against the property so that if you fail to pay the EMIs, the lender can sell your property to recover the loan amount. Have the date, time, and location of the foreclosure sale; the property address; the trustee’s name, address, and phone number; and a statement that the property will be sold at a public auction. You can authorize a lawyer, HUD-certified housing counseling agency, or other advisor to talk on your behalf with the lender about ways to avoid foreclosure. You cannot be forced to accept any plan that your representative and the lender come up with during that discussion.

Avoid Foreclosure

If the borrower completely misses the payment , the foreclosure process can begin. Usually, borrowers are given a grace period to make up any missed payments and are typically charged fees on top of whatever money is owed. Power of sale is typically the worse method between the two for homeowners, since it limits the amount of time they have before a foreclosure sale occurs.

These charges will have to be added while making the foreclosure payment. So, you will have to pay the above foreclosure charges if you are closing your loan before the expiry of the tenure. It might not be possible to pre-close the loan within the first few months of the repayment cycle. Depending on the lender you have selected, there can be a lock-in period of years for using the pre-closure facility. Not only does Home Loan foreclosure save you a substantial portion of your home loan interest, but individual borrowers with floating rate Home Loans can also do so at zero additional costs. Use our "frequently asked questions" section to learn everything about mortgages, refinancing, home equity lines of credit and more.

Nonetheless, since compliance with the foreclosure process can greatly impact the length, cost and outcome of these actions, a solid understanding of the foreclosure process is critical. Ensure that you collect a No Objection Certificate and a Home Loan foreclosure letter, confirming that your loan has been diligently repaid. Bajaj Housing Finance issues the foreclosure letter 21 days after the foreclosure request. Foreclosure action is the legal proceedings initiated by a lender in the case of mortgage default. Pre-foreclosure refers to the early stage of a property being repossessed due to the property owner’s mortgage default.

Through forbearance, homeowners are given either a temporary suspension or temporary reduction of their monthly mortgage payments. The idea is to allow them a grace period to try to get their finances back on track, without having to worry about their mortgage payments. Forbearance is surprisingly helpful for many, particularly those who lost their jobs and could use the period of no mortgage payments to hunt for a new source of income without worry. Refinancing a mortgage has always been a way for homeowners to attempt to replace their current mortgages with home loans that are more affordable. As it pertains to foreclosures, refinancing is a preventative measure that would have to be taken long before things get out of hand. It takes a quick-witted homeowner to discern when refinancing can help them avoid foreclosure.

Non-judicial foreclosure auctions are often more expedient, though they may be subject to judicial review to ensure the legality of the proceedings. Lenders can foreclose on a home through either the judicial foreclosure process or power of sale, depending on the state in which the home is located. Either way, when a borrower is delinquent with their mortgage payments and is notified of an impending foreclosure, they must act fast to prevent that result from occurring. Luckily, there are a few things that homeowners can do to avoid foreclosure. Those states which use a mortgage to evidence a lender’s security interest in property utilize a judicial foreclosure process.

If you want to pre-close a Home Loan availed on a fixed interest rate, you will have to pay the penalty for using this facility. You can check the applicable prepayment charges on the lender’s website. However, no such penalties are applicable on prepaying a floating interest rate Home Loan.

No comments:

Post a Comment